Current Location:Home

>

News

>

Market information

> Polyether market research: the overall growth trend of Global Polyether production capacity, large differences in profit levels among enterprises, stricter supervision and regulation of industry order

[Market information]:Polyether market research: the overall growth trend of Global Polyether production capacity, large differences in profit levels among enterprises, stricter supervision and regulation of industry order

Read: 373

Time:52months ago

Source:

Polyether the main raw materials of propylene oxide, styrene acrylic nitrile and ethylene oxide are downstream derivatives of petrochemical industry. The price fluctuates frequently due to the influence of macro-economy and supply and demand, which leads to plus-sized difficulty of cost control in Polyether industry. Although the price of propylene oxide is expected to decline due to the influence of concentrated new production capacity in 2022, the cost control pressure brought by other major raw materials still exists.

Unique Business Model of Polyether industry

the cost components of Polyether products are mainly direct materials such as propylene oxide, styrene, acrylic nitrile, ethylene oxide, etc., and the above raw material supplier structure is relatively balanced, state-owned enterprises, private enterprises and joint ventures all occupy a certain proportion of production scale, so the upstream raw material supply market information of the company is relatively transparent. In the downstream of the industry, polyether products have a wide range of application fields, and customers show the characteristics of large quantity, dispersion and diversified demand. Therefore, the industry mainly adopts the business model of "fixed production by sales.

Technical level and characteristics of Polyether industry

currently, the national recommended standard for Polyether industry is GB/T12008.1-7, but each manufacturer is implementing its own enterprise standards. Due to the differences in formula, technology, key equipment, process route and quality control, the same kind of products produced by different enterprises have certain differences in product quality and performance stability.

The technical level of Polyether industry in our country generally lags behind that of developed countries, but some enterprises in the industry have mastered the key core technologies through long-term independent research and development and technology accumulation, the performance of some of its products has reached the advanced level of similar foreign products.

Competition Pattern and marketization degree of Polyether industry

(1) competition pattern and marketization degree of international Polyether industry

during the 10th Five-Year Plan period, the Global Polyether production capacity showed an overall growth trend. The main concentration of capacity expansion was Asia, of which China had the fastest capacity expansion and was an important Polyether production and marketing country in the world. China, the United States and Europe are not only the major Polyether consuming places in the world, but also the major Polyether producing places in the world. From the perspective of production enterprises, at present, the Polyether production plant in the world is large in scale and concentrated in production, mainly in the hands of several large multinational companies such as BASF, kostron, Dow Chemical and Shell.

(2) competition pattern and marketization degree of domestic Polyether industry

china's polyurethane industry began in the late 1950 s and early 1960 s. In the early 1960 s, polyurethane industry was in its infancy. In 1995, China's Polyether production capacity was only 100,000 tons/year. After entering the 21st century, the quality of Polyether products has been continuously improved and the production capacity has increased year by year through the introduction of devices, independent research and development and continuous digestion and absorption of technology. Since 2000, with the rapid development of domestic Polyurethane Industry, a large number of new Polyether factories have been built in China, polyether devices have been expanded, and the production capacity has also been increasing continuously. Polyether industry has become a Industry with rapid development in China's chemical industry.

Changing Trend of profit level in Polyether industry

the profit level of Polyether industry is mainly determined by the technical content of products and the added value of downstream application fields, and is also affected by factors such as fluctuations in raw material prices.

In the Polyether industry, due to the differences in scale, cost, technology, product structure and management, the profit levels of enterprises are quite different. Enterprises with strong research and development ability, good product quality and large-scale operation usually have strong bargaining power and relatively high profit level due to their ability to produce high-quality and high-added products. On the contrary, the profit level of Polyether products with homogenization competition trend will remain at a low level, even continuously declining.

Strong supervision of environmental protection and safety supervision will standardize the industry order

the "14th five-year plan" clearly puts forward that "the total emission of major pollutants continues to decrease, the ecological environment continues to improve, and the ecological security barrier is firmer". Increasingly strict environmental protection standards will increase the investment in environmental protection of enterprises, force enterprises to reform production technology and strengthen the comprehensive recycling of green environmental protection production technology and materials. To further improve production efficiency and reduce the generation of "three wastes", and improve product quality and added value. At the same time, the industry will continuously eliminate backward high energy consumption, high pollution production capacity, production technology and production equipment, making it have a clean ring.

Enterprises that guarantee production technology and leading R & D strength stand out, and promote the acceleration of industrial integration, so that enterprises can continuously develop in the direction of intensification, and finally promote the healthy development of chemical industry.

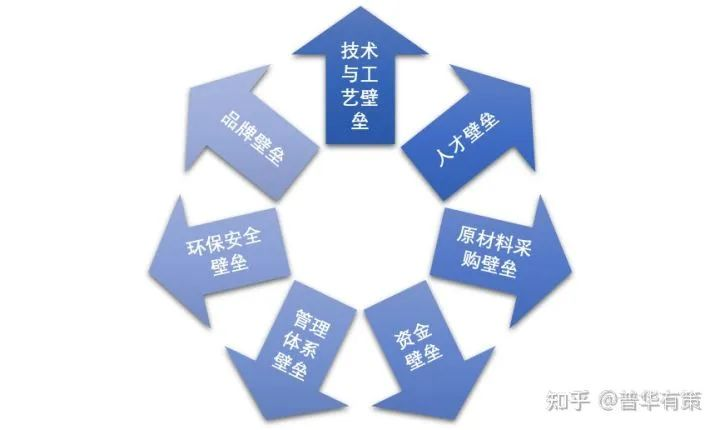

Composition of seven barriers in Polyether industry

source: Puhua youce

(1) technical and technological barriers

with the continuous expansion of the application field of Polyether products, the requirements of downstream industries for Polyether are gradually showing the characteristics of specialization, diversification and personalization. The chemical reaction process route selection, Formula design, catalyst selection, process technology and quality control of Polyether are all very critical and have become the core elements for enterprises to participate in market competition, the formation of these factors often requires long-term technological accumulation and continuous innovation. With the country's increasingly strict requirements on energy conservation and environmental protection, the industry will develop in the direction of environmental protection, low carbon and high added value in the future. Therefore, mastering key technologies is an important barrier to enter the industry.

(2) talent barrier

the chemical structure of Polyether is fine, and minor changes in its molecular chain will cause changes in product performance, so it has strict requirements on the accuracy of production technology., this requires enterprises to have high-level talents in product research and development, process research and development and production management. The application of Polyether products is relatively strong. It not only needs to develop characteristic products for different application fields, but also requires to be able to adjust the structural design at any time with products in downstream industries and to be equipped with professional after-sales service talents.

Therefore, the industry has higher requirements for professional and technical talents. Besides having a solid theoretical foundation, it also needs rich research and development experience and strong innovation ability. At present, domestic professionals with solid theoretical foundation and rich practical experience in this industry are still scarce. Generally, enterprises in this industry will combine the continuous introduction of talent teams with follow-up training, and improve their core competitiveness by establishing a talent mechanism suitable for their own characteristics. For new enterprises in the industry, the shortage of professional talents will form barriers to entry.

(3) raw material procurement barriers

propylene oxide is an important raw material in chemical industry and belongs to hazardous chemicals. Purchasing enterprises need to have safety production qualification. Meanwhile, domestic propylene oxide suppliers are mainly large chemical enterprises such as Sinopec Group, Jishen Chemical Industry Co., Ltd., Shandong Jinling, Wuyan Xinyue Chemical Co., Ltd., Binhua Co., Ltd., Wanhua Chemical, Jinling Huntsman, etc. When selecting downstream customers, the above enterprises prefer to cooperate with enterprises with stable consumption capacity of propylene oxide, form an interdependent relationship with their downstream users, and pay attention to the long-term and stability of cooperation. When new entrants in the industry do not have the ability to consume propylene oxide stably, it is difficult for them to obtain stable supply of raw materials from production enterprises.

(4) capital barriers

the capital barriers in this industry are mainly reflected in three aspects: the first is the necessary investment in technical equipment, the second is the production scale needed to achieve economies of scale, and the third is the investment in safety and environmental protection equipment. With the acceleration of product upgrading, the improvement of quality standards, the individualization of downstream demand and the improvement of safety and environmental protection standards, the investment cost and operation cost of enterprises are constantly rising. For new enterprises entering the industry, they must reach a certain economic scale in order to compete with existing enterprises in equipment, technology, cost, talents and other aspects, thus forming the capital barrier of the industry.

(5) management system barriers

the downstream application of Polyether industry is widely and dispersed. The complex product system and the diversity of customer needs have higher requirements on the operation ability of the supplier's management system. The supplier's services, including R & D, testing, production, inventory management and after-sales, all need reliable quality control system and efficient supply chain to support. The above management system requires long-term experiments and a large amount of capital investment, which constitutes a great barrier to entry for small and medium-sized Polyether production enterprises.

( 6) ring safety Barrier

china implements the approval system for chemical enterprises, and the establishment of chemical enterprises must meet the prescribed conditions and be approved before they can engage in production and operation. The main raw materials of the company's industry, such as propylene oxide, are hazardous chemicals. Enterprises must go through complicated and strict procedures such as project approval review, design review, trial production review and comprehensive acceptance when entering this field, and finally obtain the relevant license book before the official production.

On the other hand, with the development of social economy, the national requirements for safe production, environmental protection, energy conservation and emission reduction are getting higher and higher, polyether enterprises with poor profitability will be unable to bear the increasing safety and environmental protection costs and gradually withdraw. Investment in safety and environmental protection has become one of the important barriers to enter the industry.

(7) brand barriers

the production of polyurethane products generally adopts one-time molding process. Once the Polyether as raw material has problems, the whole batch of polyurethane products will have serious quality problems. Therefore, stable quality of Polyether products is often a priority for users. Especially for customers in the automobile industry, they have strict auditing procedures for product testing, assessment, certification and selection, and need to pass small batch, multi-batch and long-time experiments and trials. Therefore, the establishment of brand and the accumulation of customer resources require long-term and large amount of comprehensive resource investment, and it is difficult for newly entered enterprises to compete with the original enterprises in brand and other aspects in the short term, so as to form a relatively strong brand barrier.

Source: Puhua youce* Disclaimer: the content contained is from public channels such as the Internet and WeChat public accounts. We maintain a neutral attitude towards the views in this article. This article is for reference and communication only. The copyright of the reprinted manuscript belongs to the original author and organization. If there is any infringement, please contact Huanyi world customer service to delete it.

Mainly

Mainly

Polyurethane

Polyurethane

Fine Chemical

Fine Chemical

.png)